How to Make Money with Boring Coca-Cola in 2025

Playing this cash cow, avoiding dividend withholding taxes, and targeting a 7-8% annualized return

We’ll talk about our 2025 strategy in our upcoming webinar next week, but here’s another stock we’re highly excited about. Excited because it’s boring, overlooked, defensive, and able to make us a 7-8% annualized return.

And if our bullish assumption becomes reality, we’ll be making roughly 11-12%. That would be a decent return for such boring stock. All while reducing our downside risk notably, and keeping excess cash for shorter-term opportunities.

We’re talking about Coca-Cola, the proven Dividend King with reliable free cash flow. It’s currently generating a 3.1% dividend yield, and that dividend has been quite important over the past few years. Right now, we prefer Coca-Cola over PepsiCo (see further commentary below).

Foreign investors often encounter the challenge of facing significant dividend withholding taxes twice. This is where options can offer a valuable advantage, as they price in future dividend streams without incurring tax consequences. Additionally, foreign investors might approach forward returns on U.S. equities with caution, especially in light of the recent strength of the dollar. With a stock replacement strategy, your net exposure to foreign FX will be reduced notably.

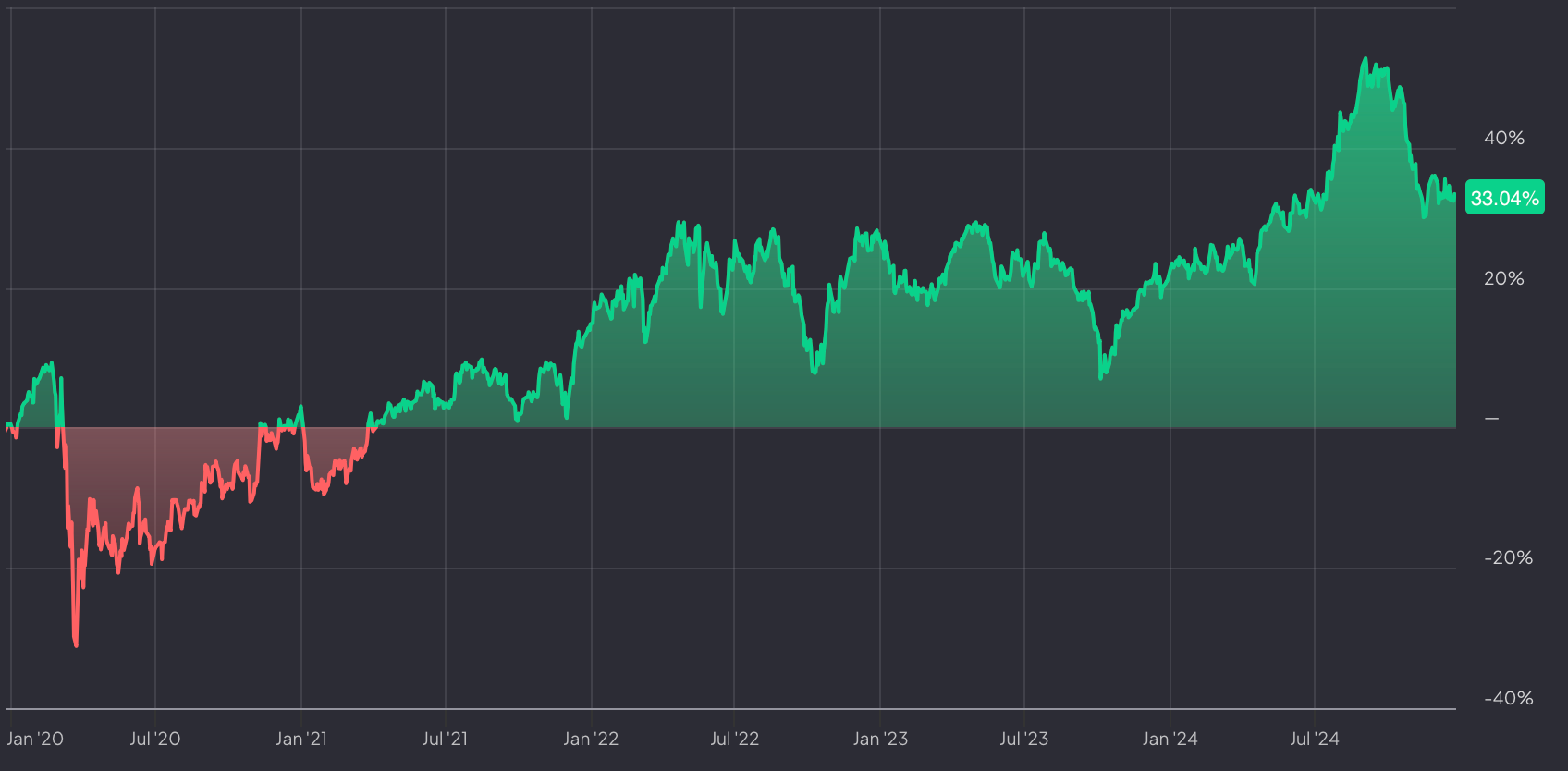

Price Return Coca-Cola

Still, over the past few years, Coca-Cola has been lagging the market, as it’s far from fancy and not a tech stock. That’s perfectly fine for our strategy: maximizing returns in a sideways market, while protecting our downside risk (anything can happen).

Total Return Coca-Cola

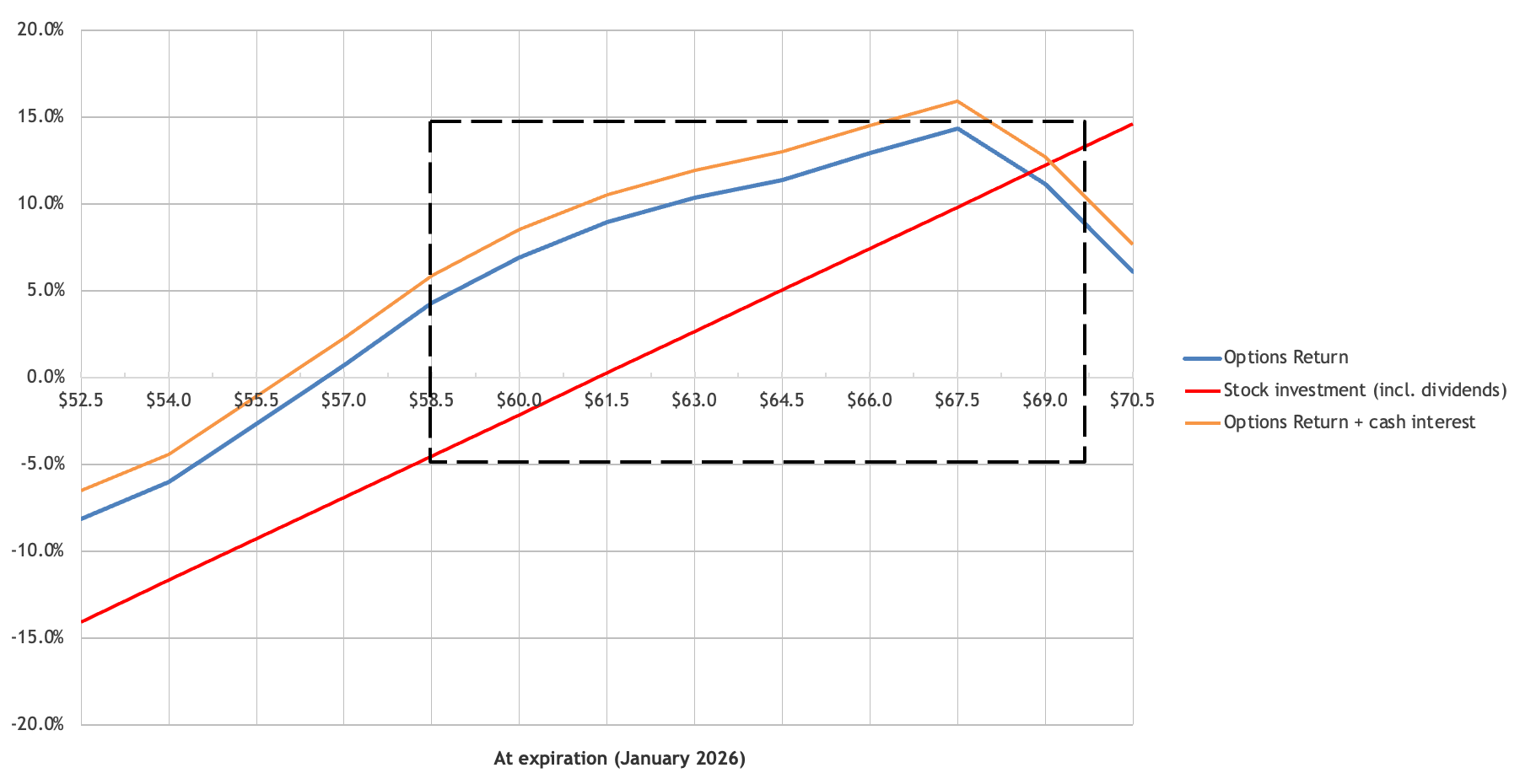

The setup we’re going to execute later today (KO has very tight options spreads) has the following pay-off (12.5 months). In terms of total return for its shareholders, we’re expecting Coca-Cola to earn -5% to +11%, which would be a typical range of expectations.

The stock’s trading a roughly 19x next year’s NOPAT, which isn’t excessive, though not excitingly cheap either. Also, there’s been a bit of noise in its cash flow statement as of late (see below), and US companies face potentially significant FX headwinds in FY25. These factors make us neutral to moderately bullish for next year (and likely beyond 2025 as well). Overall, quite some puts and takes that make it relatively “unloved” when there’s AI, and other momentum trades to choose from. That’s how we like it.

If Coca-Cola surpasses our expectations and delivers an +18% return, we’re satisfied with a 9.5%. It’s a straightforward trade-off driven by probabilities. There’s no such thing as a free lunch - you can’t fully capitalize on a rising market while also securing sizable returns in a sideways or moderately declining one.

But let’s say that we’re completely wrong, and for whatever reason Coca-Cola were to crash 32% in one year. Whether it be a global financial crisis, the passive investing bubble bursting, loss-weight drugs hitting its sales and profitability, you name it.

Assuming we get a slight uptick in implied volatility (from 17.5%/18% to say 24%), we’ll be losing 2-3% after accounting for excess cash earning a 3% yield over the next 12.5 months.

However, that excess cash provides us ample opportunities if the market’s dropped 20% and we’re able to buy the dip elsewhere (also through basic options strategies like a cash-secured put). Now all of a sudden, it’s entirely possible to break-even with the market down 30%.

That’s the purpose of the Theta Tortoise - don’t expect home runs of 15, 20, 30% a year. But singles and doubles of 5% to 9% with significantly lower market exposure and thus lower risk. And if the s*** hits the fan, the strategy provides a true hedge during stormy times.

Let’s take a closer look at the strategy.

Our Transactions and Portfolio

We’ll be sharing the spreadsheet with our current options positions and transactions tomorrow morning (on the “Our Portfolio” page). The idea is to translate our real-life positions to a starting portfolio value of 200,000 USD. That way, more investors can follow along, and adjust accordingly based on their personal portfolio size, and risk appetite.