Doing the Opposite from What Everyone Else's Doing

More color on the opportunity of selling premium when it's priced attractively

Time for another research article that’s extremely relevant during market doldrums. Yet again, a blog on implied volatility and its tale on how risk and reward is priced. We wrote several blogs on this topic already.

As we put this article out, the portfolio value hit a new all-time high by doing what it’s been doing for several weeks: registering bi-weekly moves of .2% - .4% and carrying significantly lower risk vs. the market. This is completely different from an index fund that has unlimited upside potential, while we play a game of sizing our portfolio whenever the opportunity is bigger and taking advantage of the passage of time.

Rotation

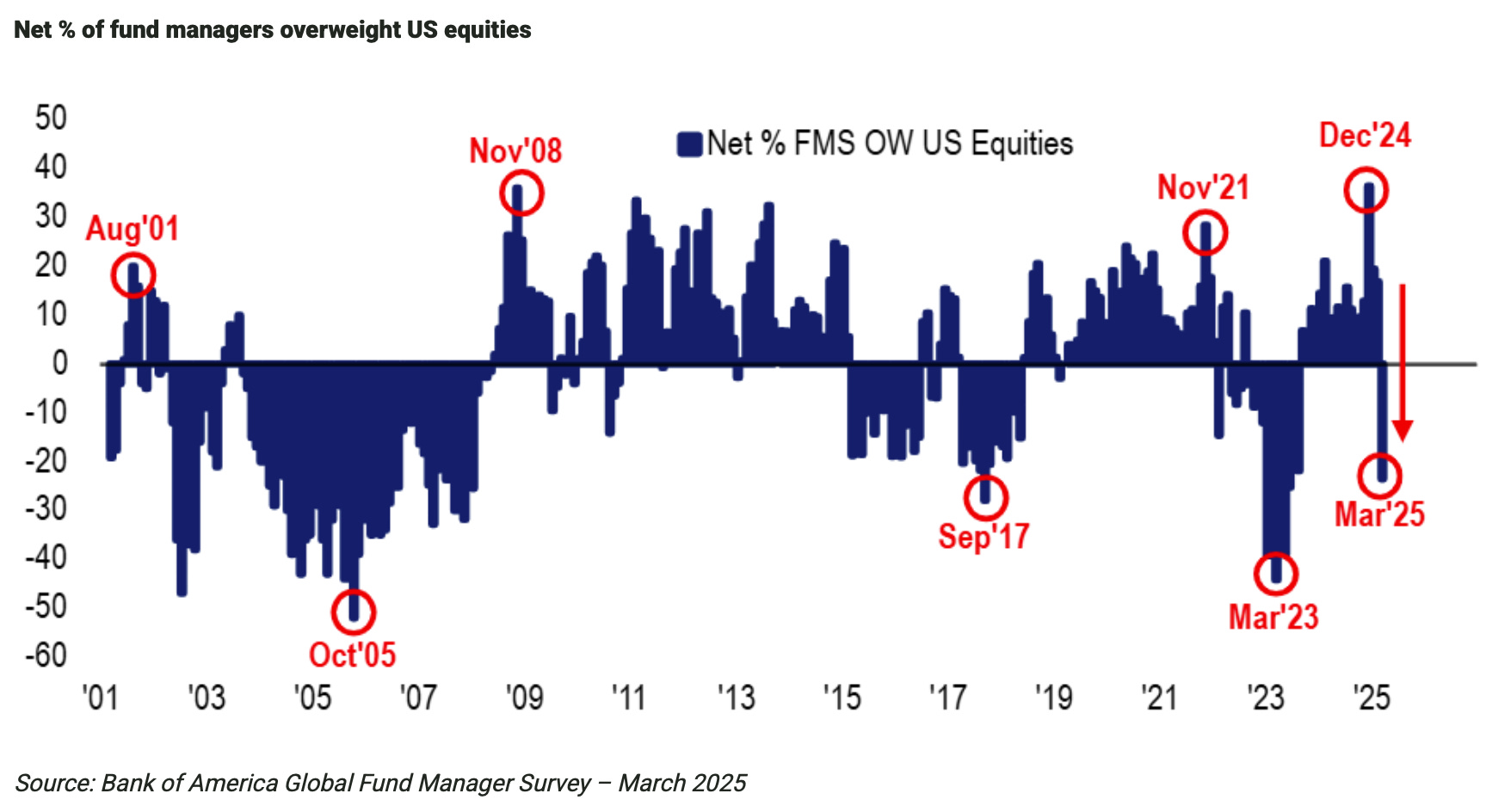

And today’s price action is interesting. US professional investors have been selling out of US stocks at the fastest pace on record. Meanwhile, cash levels remain near historic lows, indicating there’s been a shift toward other countries and assets (like Germany, gold, Chinese tech).

Interestingly, even retail investors didn’t buy the dip over the past few weeks.

Orderly Pullback

What could one usefully deduce from this, now that the VIX has gone down from 29% (close to 30%) to 20.8% today? It’s been a pretty orderly pullback, and as we said in last weekend’s webinar, we expect investors who cherry pick strong quality names should do well if this no man’s land environment persists for several months/quarters.

That’s exactly because the market hasn’t rebounded since the VIX’s contracted by 9 points. Put another way, the sellers got out, and are now looking at where and when to re-enter, likely awaiting a further drop in the VIX index below 20%. Given that the VIX has already dropped to less fearful levels, a new down move is still likely, but again: an orderly pullback doesn’t lead to an “all-sell” situation.

So to be clear, by no means are we suggesting that all’s clear, but the narrative of buying the dip and praying for the best has changed, and that by itself is a good thing. We’re not contrarian stock pickers in that we go for deep value, turnarounds… but proven quality stocks with high Sortino ratios (high return per unit of downside risk taken).