7 Buys for Conservative Investors (January)

With decent options premiums to optimize your break-even

Over the past one month, some quality stocks have come down quite a bit. Unsurprisingly, our members ask us: which stocks are deemed attractive?

Let’s take a closer look at 7 attractively priced stocks for conservative investors and the opportunity to sell options premium. A healthy blend of quality, growth, defensiveness, exceptional managers, and boring businesses. That’s how a Tortoise wants to win the race: slow and steady.

The sheet with our basic calculators for covered-calls and cash-secured puts can be downloaded at the end of this post. Note: below mentioned prices as of Jan 6, at market-close.

1. Coca-Cola

Coca-Cola is a proven Dividend King with reliable free cash flow. It’s currently generating a 3.1% dividend yield, and that dividend has been quite important over the past few years. Right now, we prefer Coca-Cola over PepsiCo (see further commentary below).

The stock’s trading a roughly 18.5x next year’s NOPAT, which isn’t excessive, though not excitingly cheap either. Also, there’s been a bit of noise in its cash flow statement as of late (see below), and US companies face potentially significant FX headwinds in FY25. These factors make us neutral to moderately bullish for next year (and likely beyond 2025 as well). Overall, quite some puts and takes that make it relatively “unloved” when there’s AI, and other momentum trades to choose from. That’s how we like it.

Many investors are now looking at PepsiCo, so you may be wondering: why not pick PepsiCo over Coke? Pepsi’s forward earnings multiple’s dropped quite a bit (in fact, it hit the lowest since pandemic), but there are a couple of factors we’d like to point out.

We’ve been warning about PepsiCo’s cash flow and allocation policy on our private Discord (The Compounding Tortoise). PepsiCo’s net working capital is negative, which is great as long as you have good volume growth and pricing. Yet, the former has turned south (including Pepsi’s highly profitable Frito Lay North America). Adding recent moderation in pricing, PepsiCo’s cash flow has been under quite a bit of pressure.

So, what you’re looking at is negative growth in cash flow from operations (it’s been going on for a while now). Meanwhile, CAPEX are increasing at a time when volume growth remains sluggish, and CAPEX are being done at decreasing incremental returns.

At the same time, cash dividends are exceeding total free cash flow, meaning that incremental borrowing is likely to push PepsiCo’s interest charges up…

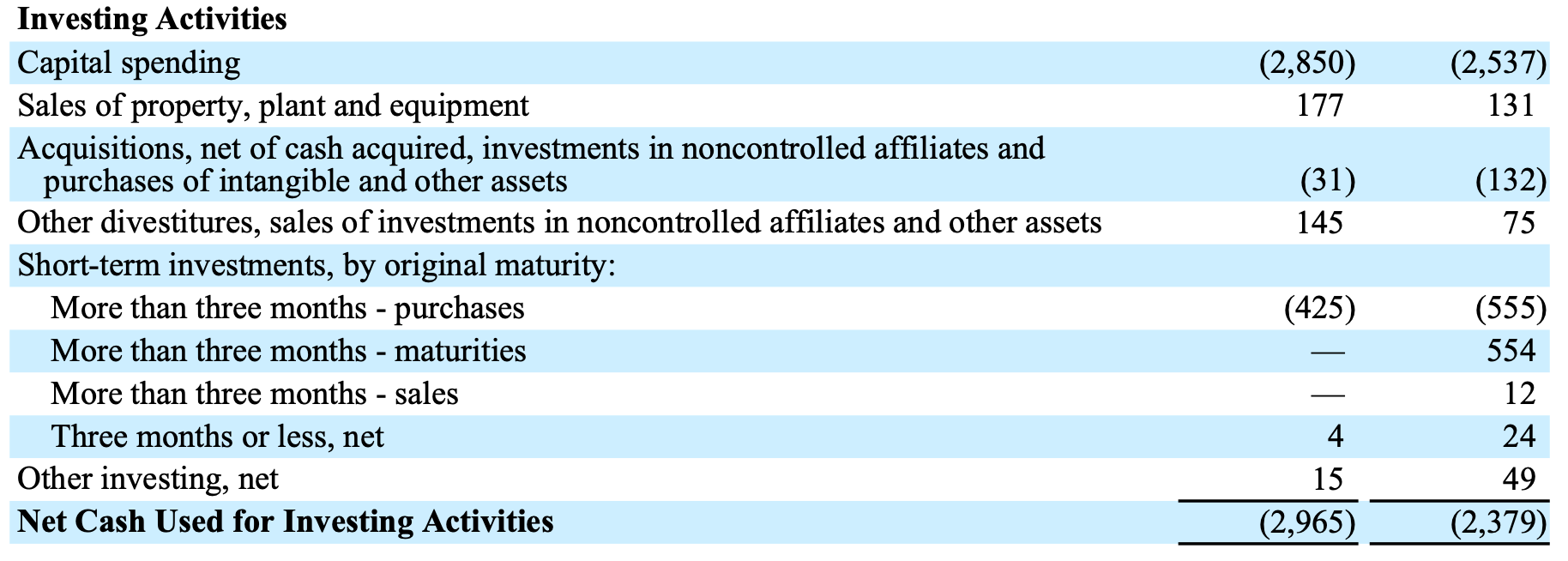

With Coca-Cola, recent cash flow headwinds are related to a one-time ongoing tax litigation impact from the IRS (6.0 billion USD).

Overall, we’d say Coca-Cola’s cash flow resilience, lower capital intensity, growing market share in nonalcoholic beverages, and operating margin expansion (more feasible compared to PepsiCo) warrant a premium over PepsiCo.

In Q3, Coke reported decent top and bottom line growth, adjusted for non-operating items (such as earn-out revaluations related to prior M&A).

Net revenues declined 1% to $11.9 billion, and organic revenues (non-GAAP) grew 9%. Revenue performance included 10% growth in price/mix and a 2% decline in concentrate sales. Concentrate sales were 1 point behind unit case volume, primarily due to the timing of concentrate shipments.

Let’s say you want to make some money with Coca-Cola, but don’t want take on full equity exposure (and thus risk) right from the start. Additionally, should the stock drop, you can potentially buy it at a nice discount. Sell a cash-secured put.

In that case, we’re obliged to potentially buy the stock at a predetermined price, known as the strike price, by a certain date, known as the expiration date. It all depends on where the stock’s trading at expiration. There could be early assignment (i.e. you ending up buying the stock earlier than the expiration date), but that’s rare and relates to where the stock’s trading relative to the strike price (in-the-money), and any upcoming ex-dividend date.

In return for undertaking this contract obligation, and because of the unknown timing of potential assignment (will we end up owning the stock), we get paid a cash premium. If nothing happens (i.e. no assignment) with the passage of time, we’ll keep the cash premium. And if we get assigned, we own the stock at a lower price, plus adjusted for that cash premium received.

The beauty of a cash-secured put is that your break-even is lower, and even if you get hit by expiration, you’ll end up owning an attractively priced stock at an even more attractive price.

The February 21, 2025 $57.50 put on Coca-Cola gets us to a 6.8% annualized return, with the break-even point at $57.03 vs. owning the stock outright at $60.81.

Based on our internal and third-party research, selling a put when volatility is decent (VIX of 16-19%) or high (>20%) yields strong risk-adjusted and absolute returns (if you’re shooting for 6-8% per annum). Also, we’re looking for stocks with relatively limited downside, and maybe, stocks where there’s no real catalyst for an up or down move. Overlooked quality stocks are perfect for a sideways to moderately bullish options strategy that benefits from the passage of time.

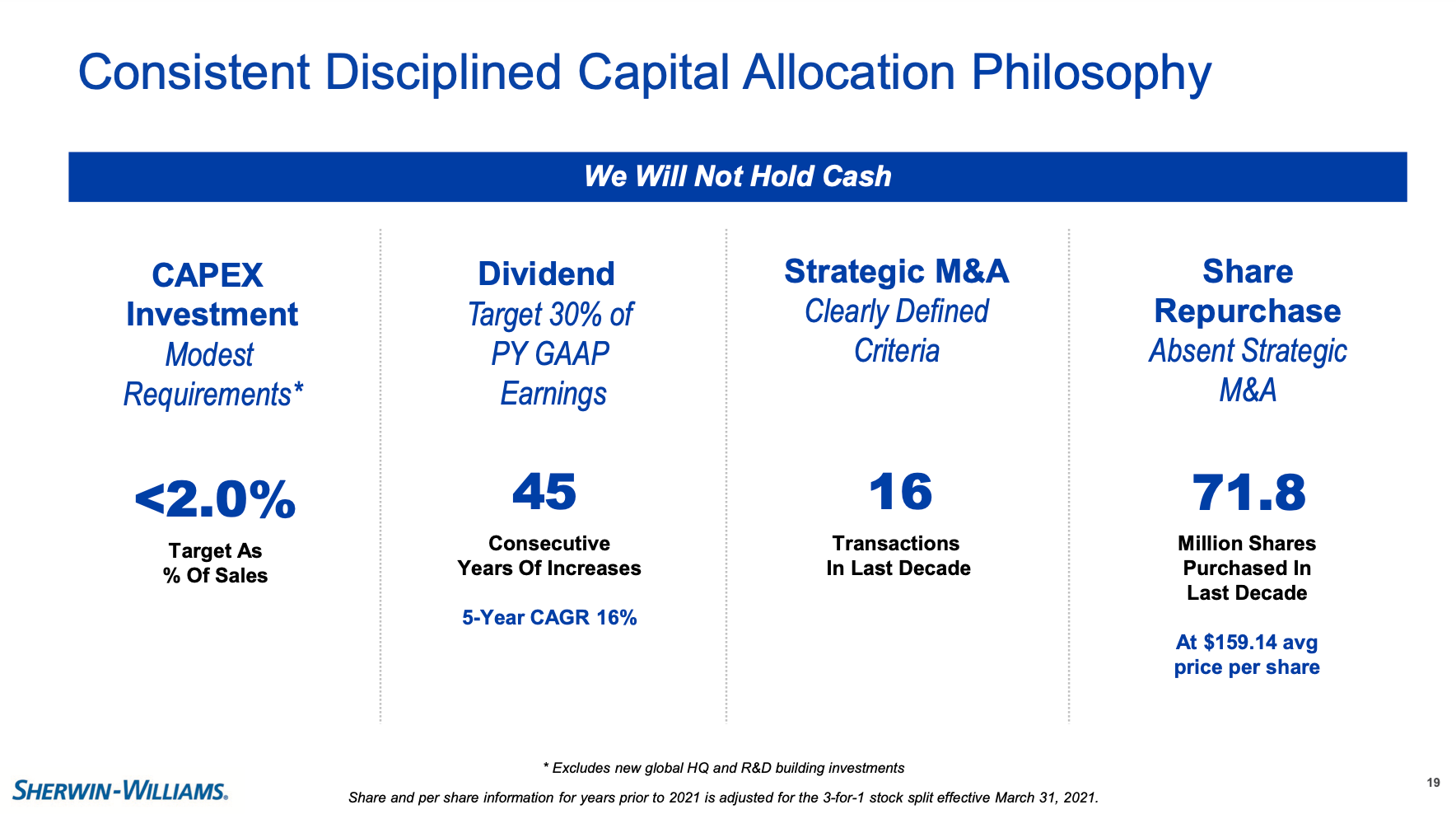

2. Sherwin-Williams

Sherwin-Williams is a diversified conglomerate with a portfolio that extends well beyond its flagship brand. Its notable subsidiaries include Valspar (paints, stains, and sealers), Minwax (wood finishes), Purdy (paint tools and accessories), Krylon (spray paints), Thompson's WaterSeal (multi-surface sealers and cleaners), Cabot (stains and bleaching oils), Ronseal (wood stains and paints), and several others.

The company also manufactures corrosion-resistant coatings designed for commercial vessels and the marine industry, offering protection against harsh and humid environments. With a customer base spanning residential, commercial, and industrial sectors, Sherwin-Williams maintains a diversified business model that helps mitigate the impact of cyclical end markets.

For instance, while Home Depot is experiencing stagnating sales due to declining home sales and reduced spending on home improvement, Sherwin-Williams is less reliant on consumer-driven trends. Although the company benefits from a strong housing market and increased demand for home improvement and DIY projects, its broad business scope ensures that its performance is not entirely tied to consumer spending patterns.

The stock’s very rarely on sale, and the recent drop might prove an attractive entry point. Implied volatility has been ticking higher. As such, those looking to get paid in advance for buying the stock at an even larger discount by the end of February should watch the $310 put. After factoring in the cash premium of $3.10 (mid-price), total break-even is at $306.90. Not bad at all for a company with pricing power and improving comps for this year. And if we don’t drop, you’ve made an annualized return of roughly 9%.

Let’s take a look at the other 5.